Risk Management Live

Manage trading positions, calculate risk sensitivities and price financial instruments in the browser.

Price Forwards, Europeans and Americans using the pricing tool

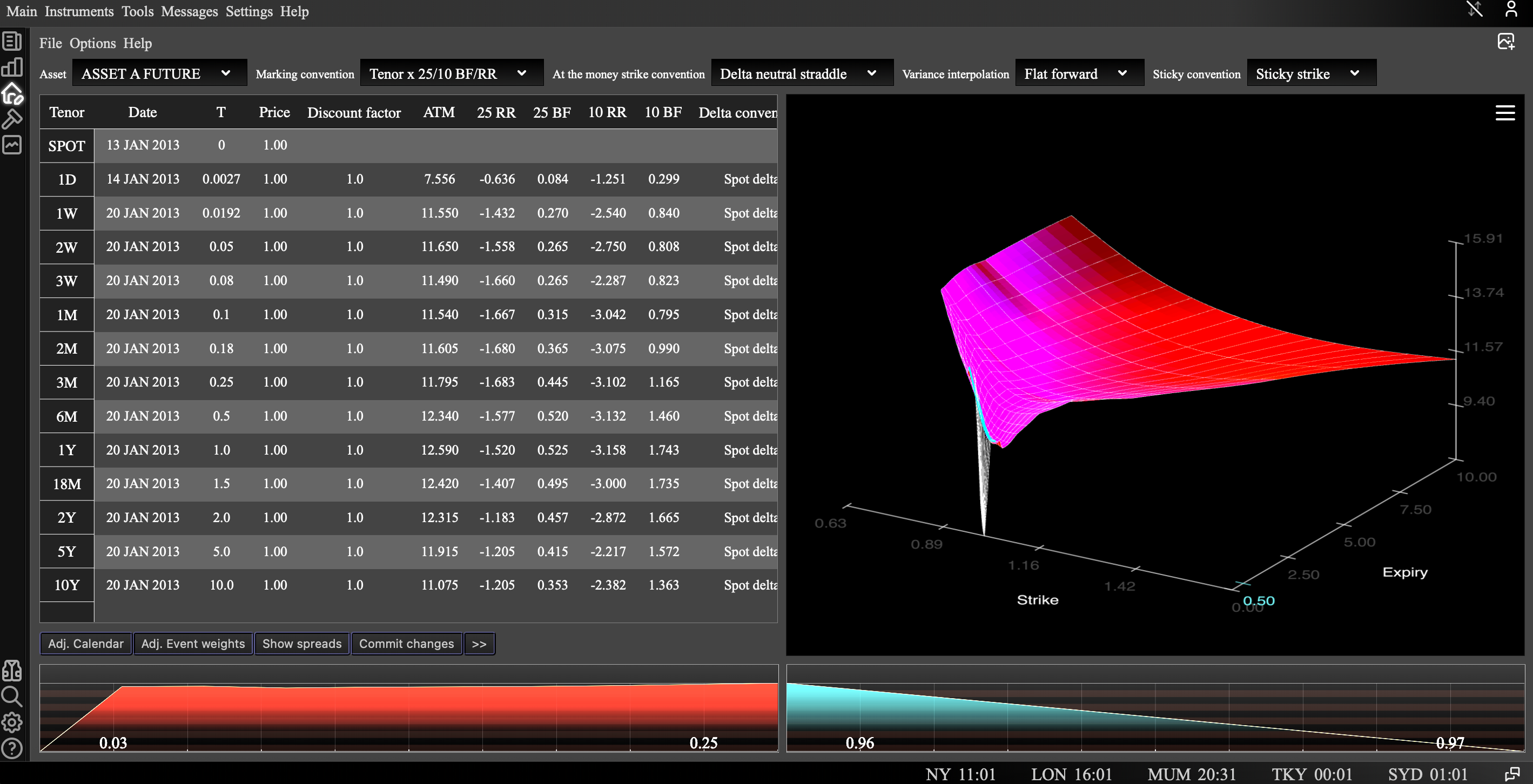

Mark implied volatility surfaces with the market editor tool

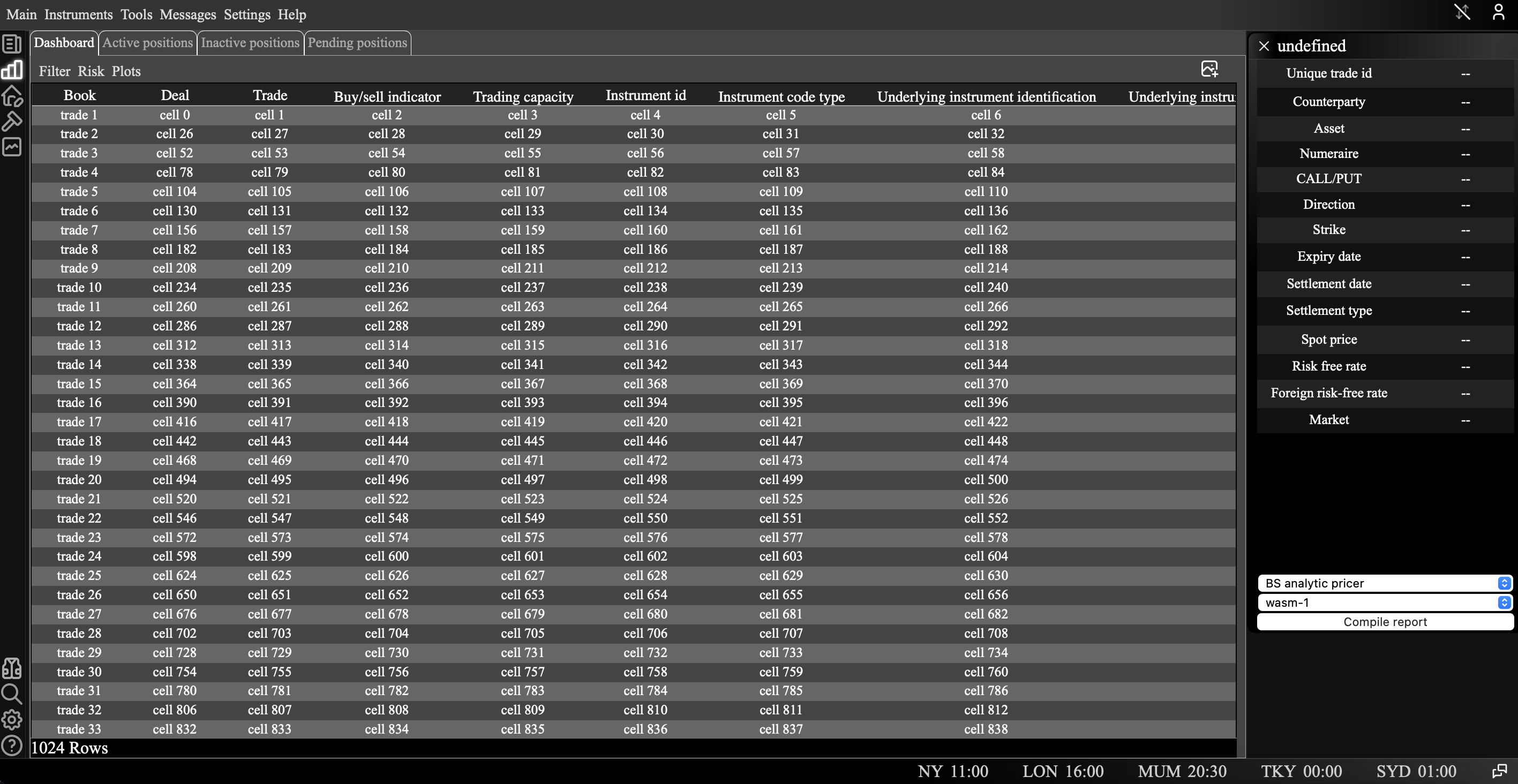

Manage trades with the portfolio book viewer

Pricing

Retail

- Standard models: Black-Scholes, Heston, Dupire and SABR.

- Basic instruments: Forwards, Europeans and Americans.

- Popular strategies: butterflies, risk reversals and straddles.

Retail Plus

- Includes all features of Retail.

- More advanced models: Heston LSV and rough Heston.

- Additional instruments: digitals/binaries and touch options.

Small Team

- Includes all features of Retail Plus.

- Licence covers up to six users.

- Supports team collaboration features such as sharing volatility surface and trading instrument data.

Enterprise

- Includes all features of Small Team.

- Supports custom payoff functions.

- Advanced compute for large portfolios.